The New Tariff Landscape: Understanding the 125% Increase

When President Trump announced the sweeping tariff changes earlier this month, the seafood industry immediately recognized the game-changing implications. Unlike the other 75 countries granted a 90-day grace period with a temporary 10% flat rate tariff, China received no such reprieve. Instead, Chinese seafood products were hit with an immediate and substantial 125% additional tariff.

For Chinese tilapia exports, which had already been operating under a 25% tariff since 2018, this new development brings the total duty to a staggering 150%. Landy Chow, marketing manager at Siam Canadian, didn’t mince words when describing the situation: “With a 125% additional tariff, things will be even more serious. That is extremely too high.”

The impact has been swift and severe across China’s major processing hubs like Qingdao and Dalian. Industry sources report that virtually all US-related orders have been suspended, creating an unprecedented standstill in what has historically been one of the most interdependent segments of US-China trade.

See another post: How to Identify High-Quality Frozen Tilapia Fillets A Complete Guide for Importers -> Click here

Tilapia Industry: Current State and Immediate Impact by Chinese Tilapia US Tariff

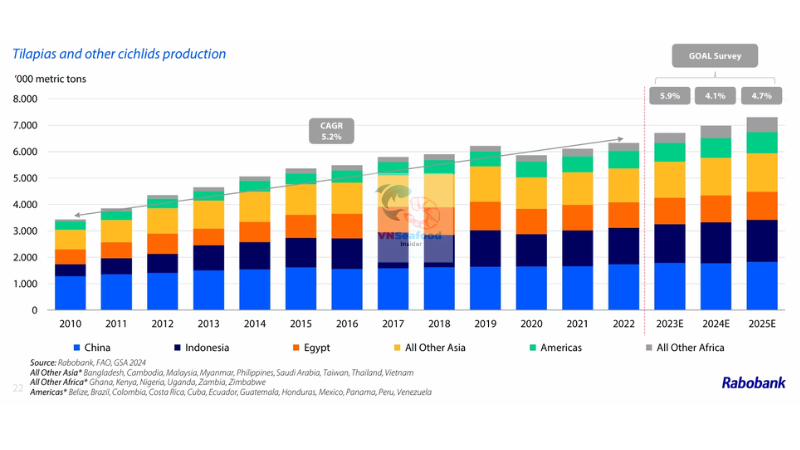

Prior to this tariff announcement, China dominated the US tilapia market despite the existing 25% duty. Chinese producers had adapted to the 2018 tariff increase, managing to maintain a significant market share through production efficiencies and scale advantages. However, the leap from 25% to 150% represents a fundamentally different challenge—one that many industry experts believe is insurmountable in the short term.

The Chinese tilapia sector was already facing significant domestic challenges before this tariff bombshell:

- Recovery from typhoon damage in early 2024

- Implementation of stricter emissions regulations

- Increasing labor costs compared to Southeast Asian competitors

- Transportation and logistics challenges amid global supply chain disruptions

With the new tariff structure, Chinese exporters are reporting that their US business has effectively vanished overnight. Even long-standing processing arrangements involving US-caught fish (particularly Alaskan species) being processed in China and re-exported to America have been thrown into disarray.

“No one even checks if it’s 125% or 145% anymore,” shared one Qingdao exporter in a recent industry communication. “All we know is orders are off the table.”

The Southeast Asian Opportunity: Vietnam, Thailand, and Indonesia

As the saying goes, “When one door closes, another opens,” and this situation presents a textbook example of this principle in action.

Vietnam’s Potential Tilapia Growth

Vietnam, already a seafood export powerhouse with its dominant position in the pangasius (basa) market, stands to gain significantly from this market disruption. Currently subject only to the temporary 10% tariff rate (which could potentially rise to 46% after the 90-day grace period if no new trade agreements are reached), Vietnamese producers have a substantial competitive advantage over their Chinese counterparts.

The Vietnamese seafood industry has been rapidly developing its tilapia production capacity over recent years, with investments in both farming infrastructure and processing facilities. While current production volumes remain below China’s, the financial incentive to accelerate growth has never been stronger.

For Vietnamese producers, the challenge will be balancing the opportunity for tilapia expansion while maintaining their strength in pangasius exports. Both species serve similar market segments in the US, and importers may substitute pangasius for tilapia in many applications if pricing and availability favor the former.

See more: 5 Common Mistakes When Importing Tilapia from Vietnam

Indonesia and Thailand’s Market Position

Indonesia and Thailand also find themselves well-positioned to capitalize on this market shift. Both countries have established tilapia production capabilities, though like Vietnam, they currently produce at volumes below China’s dominant position.

These nations benefit from:

- Existing seafood processing infrastructure

- Experience with export standards and compliance

- Established logistics networks for perishable products

- Lower labor costs compared to China

However, as Landy Chow noted, “The problem is that these countries still do not produce significant amounts of tilapia at this moment.” Scaling up production will take time—time that US importers may not have if they need to maintain consistent supply for their customers.

US Market Adaptations: How Importers and Consumers Will Respond

The US tilapia fillet market, valued at approximately $1.1 billion annually, now faces significant supply chain disruption. Historically, China has supplied over 70% of America’s tilapia imports, making this tariff impact particularly acute.

Shifting Sourcing Strategies

US importers are rapidly exploring alternative sourcing options. According to industry sources, many have already begun redirecting orders to Vietnam, Indonesia, and other countries benefiting from the lower 10% temporary tariff rate.

However, this transition presents several challenges:

- Establishing relationships with new suppliers

- Ensuring consistent quality standards

- Negotiating competitive pricing

- Addressing potential capacity limitations

Some importers are adopting a hybrid approach, maintaining limited Chinese supply for premium products while shifting volume purchases to Southeast Asian sources.

Product Substitution Effects

As Chow suggested, another likely market adaptation will be increased substitution of pangasius for tilapia in many applications. Both are mild, white-fleshed fish that serve similar culinary purposes. With Vietnam’s established pangasius production capacity, this represents the path of least resistance for many importers seeking to maintain supply continuity.

For US consumers, this may manifest as:

- Menu changes at restaurants

- Different product options in retail seafood cases

- Potential price increases across white fish categories

- More product origin diversity in the frozen fish section

At VNSeafoodInsider, we anticipate that US consumers may see tilapia prices increase by 15-25% in coming months as the market adjusts to these new supply chain realities.

Long-term Industry Outlook and Strategic Considerations

While the immediate market disruption creates challenges and opportunities, the longer-term implications require strategic thinking from all industry participants.

Potential Scenarios for Chinese Producers

Chinese tilapia producers face several potential paths forward:

- Diversification of export markets: Focusing more intensively on non-US destinations like the EU, Middle East, and domestic consumption

- Production relocation: Establishing operations in countries not subject to the higher tariffs

- Strategic partnerships: Creating joint ventures with Southeast Asian producers

- Value-added focus: Shifting toward higher-margin products that can better absorb tariff impacts

- Waiting game: Maintaining minimal operations while hoping for eventual trade normalization

The reality will likely involve a combination of these approaches, varying by producer size and financial capacity.

Opportunity Assessment for Southeast Asian Producers

For countries like Vietnam, Indonesia, and Thailand, capitalizing on this opportunity requires careful consideration of several factors:

- Investment timing: Determining how much production capacity to add, and how quickly

- Regulatory compliance: Ensuring all production meets US import requirements

- Market positioning: Deciding whether to compete primarily on price or differentiation

- Sustainability credentials: Leveraging environmental practices as a competitive advantage

- Processing capacity alignment: Ensuring processing facilities can handle increased production

The most successful producers will be those who balance aggressive growth with sustainable business practices.

See more: Top 6 Vietnam Seafood Export Products 2024 – Market Insights and Trends 2025

Navigating Market Uncertainty: Advice for Industry Participants

If you’re involved in the tilapia supply chain—whether as a producer, processor, importer, or retailer—these rapidly changing conditions require adaptability and foresight.

For Producers and Exporters

- Maintain transparent communication with your buyers about capacity and pricing

- Accelerate certifications and compliance documentation

- Consider strategic alliances to quickly address capacity limitations

- Develop contingency plans for various tariff scenarios after the 90-day review period

- Invest in quality control to capitalize on the opportunity to establish new relationships

For Importers and Distributors

- Diversify your supplier base across multiple countries

- Evaluate product substitution options (pangasius, other whitefish)

- Communicate proactively with your customers about potential supply adjustments

- Consider longer-term contracting where available to secure supply

- Monitor political developments that might signal policy changes

A Transformative Moment for the Global Tilapia Trade under Chinese Tilapia US Tariff

The imposition of the additional 125% tariff on Chinese tilapia represents a pivotal moment for the global seafood industry. While Chinese Tilapia US Tariff created significant hardship for Chinese producers who have dominated this market for decades, it simultaneously opens doors for Southeast Asian producers ready to step into the gap.

At VNSeafoodInsider, we’ll continue monitoring this situation closely, providing you with the most current analysis and market intelligence as developments unfold. The next 90 days will be critical in determining whether this represents a temporary disruption or a permanent realignment of global tilapia trade flows.

For producers in Vietnam and other Southeast Asian nations, this moment presents a rare opportunity to capture market share in the world’s largest seafood import market. However, capitalizing on this opportunity will require both immediate action and strategic patience—building capacity while maintaining quality as the cornerstone of sustainable growth.

The tilapia on your plate may soon have a different origin story, but the global seafood industry’s resilience and adaptability ensure that supply will continue to meet demand, albeit through reconfigured channels and potentially at different price points.

Pingback: Vietnam Tilapia: The Rising White Fish Alternative Amid Global Supply Disruptions