The Global Whitefish Supply Crisis: Why Prices Are Surging in 2026

The whitefish market does not get rattled easily. Buyers are used to seasonal swings, quota adjustments, and the occasional bad fishing year. But 2026 is different. Multiple supply shocks are hitting at the same time, across different species and different oceans, and the cumulative effect is a market that feels genuinely tight.

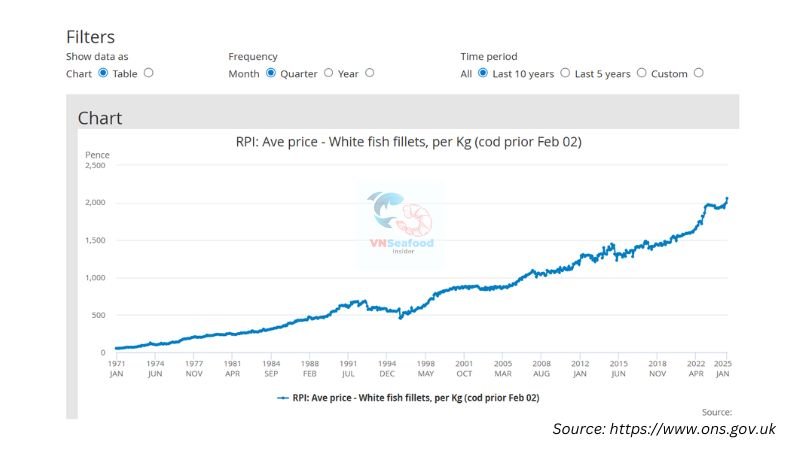

Regional wholesale prices for Atlantic cod reached record or near-record levels in late 2024 and stayed stubbornly high into 2026. Management decisions for North Atlantic whitefish stocks further lowered total allowable catches compared with 2025. The word “crisis” gets overused in commodity markets, but when importers and processors openly report difficulty securing enough volume for basic filleting operations, the shoe fits.

Alaska Pollock Season A 2026: Lower Yields Despite Similar Harvest Effort

Here is the frustrating part for pollock buyers: boats went out, they fished, and the harvest effort looked roughly the same as last year. By the end of March, about 88 percent of the Bering Sea quota had been caught. On paper, that sounds fine.

Below the surface—literally—the story was different.

Fish entered their spawning cycle earlier than expected, which weakened their body condition. Meanwhile, a higher proportion of undersized fish (200–300 grams each) showed up in catches. Smaller fish with lower body mass means worse processing yields. The math is unforgiving: pollock fillet production fell 16 percent in the Bering Sea and a painful 36 percent in the Gulf of Alaska, producing an overall statewide decline of about 18 percent. H&G products dropped 16 percent. Surimi output fell 8 percent.

Regulatory actions also restricted directed fishing in some statistical areas to avoid overshooting quotas and comply with ecosystem-based management measures. So processors received less raw material, and each tonne they did receive converted into fewer finished fillets.

For buyers who rely on affordable whitefish blocks for battered, breaded, and institutional products, this is a significant supply gap.

Cod, Haddock, and the Substitution Squeeze

Normally, when pollock gets tight, buyers pivot to cod or haddock. This year, that escape route is blocked.

Wholesale prices for H&G cod and haddock from Norway and Russia climbed to historically high levels through late 2024 and remained elevated well into 2025. Cod prices in 2026 sit more than 40 percent above year-ago levels. Haddock eased only partially from its peaks—partial relief is still expensive relief

.

Industry observers call this the “substitution squeeze.” Every major wild-caught whitefish species is either supply-constrained, price-inflated, or both. Importers who built their product lines around readily available, reasonably priced cod or pollock fillets now face a strategic question: keep paying premium prices and squeeze your margins, or find an alternative protein that can fill the same slot on the plate?

That question brings us to the Mekong Delta.

Why Importers Are Reconsidering Pangasius as Whitefish Alternative

Let us be honest. Pangasius has not always had the easiest reputation in Western markets. A decade ago, quality inconsistencies and media skepticism made some buyers hesitant. But the industry has matured considerably since then, and the current market conditions are forcing a practical reassessment.

When your usual cod supplier quotes prices that make your finance team wince, Vietnam pangasius starts looking less like a backup plan and more like a smart strategic move. The fillet is white, mild-flavored, and neutral enough in texture to work across coated, prepared, and institutional formats—exactly the applications where cod and pollock have traditionally dominated.

Pangasius vs. Cod: A Cost and Yield Comparison for Importers

Here is where the numbers do the talking.

Fillet yield from farmed pangasius is relatively high and, crucially, predictable. Unlike wild fisheries where biological variability can slash yields season to season (see: Alaska pollock, 2026), aquaculture offers consistency. The Mekong Delta’s processing infrastructure is purpose-built for export, with major facilities running multiple shifts to handle volume efficiently.

On the cost side, the current landed price per kilogram for a finished cod fillet often exceeds what price-sensitive retail and foodservice buyers are willing to pay. Pangasius fillets, even after freight and import duties, typically come in significantly lower. For buyers in the prepared and frozen segments—think fish fingers, institutional meal kits, breaded portions—this cost advantage can be the difference between a profitable product line and a money-losing one.

A quick comparison to keep in your sourcing file:

Factor Atlantic Cod (2026) Vietnam Pangasius (2026) |

Price trend | Up 40%+ YoY | Stable to moderate increase |

Supply reliability | Quota-constrained, volatile | Farm-based, plannable |

Fillet yield consistency | Variable by season | High and predictable |

Flavor profile | Mild, flaky | Mild, smooth |

Best-fit applications | Premium retail, restaurants | Coated, prepared, institutional, retail |

The bottom line: pangasius offers a favorable combination of raw-material price, yield predictability, and processing infrastructure that wild whitefish simply cannot match right now.

See more: Top 5 Exotic Vietnam White Fish That Importers Should Consider

Vietnam Pangasius Supply in 2026: Production Capacity and Export Momentum

Vietnam’s pangasius sector is not standing still. The Mekong Delta maintains over 6,000 hectares of active farming area, concentrated in Dong Thap, An Giang, Can Tho, and Vinh Long provinces. In 2025, total production reached approximately 1.67 million tonnes, and export revenue exceeded $2.2 billion USD—an 8 percent increase over the prior year.

What is particularly notable is the growth in value-added pangasius products, especially in the U.S. market. Vietnamese exporters are moving beyond basic frozen fillets into breaded portions, marinated cuts, and ready-to-cook formats. This shift positions pangasius not just as a commodity substitute but as a product category with its own retail identity.

Key Export Markets: Where Vietnam Pangasius Is Gaining Ground

The United States remains the marquee growth story, with value-added products seeing what industry observers describe as “breakthrough” demand. But the opportunity extends further. China, the EU, and several Middle Eastern markets continue to absorb significant pangasius export volumes.

For importers evaluating whitefish sourcing alternatives, this broad market footprint is actually reassuring. It means the Vietnamese supply chain is stress-tested across multiple regulatory environments, quality standards, and logistics corridors. A processor shipping ASC-certified fillets to a German retailer and HACCP-compliant breaded products to a U.S. foodservice distributor is a processor that knows how to meet demanding specifications.

For the full breakdown of certifications, processing standards, and trade regulations, check our Vietnam Pangasius: The Complete Importer’s Guide.

Challenges Facing Vietnam Pangasius Supply: What Importers Should Monitor

We would not be doing our job if we only told you the good parts. Pangasius supply has real vulnerabilities, and smart importers should understand them before committing to larger volumes.

Climate and Seasonal Heat Stress on Pangasius Farming

Right now, the Mekong Delta is deep into its hot season. Temperatures regularly hit 39–40°C. That kind of heat reduces dissolved oxygen in pond water while simultaneously increasing the fish’s oxygen demand—a bad combination that leads to stress, disease outbreaks (hemorrhagic septicemia, eye protrusion, bloating), and mortality spikes.

Farmers are adapting. Standard practices now include raising pond water levels, increasing aeration, and frequent water quality monitoring. Feed rations get cut by 30–70 percent on days above 35°C to reduce metabolic load. Vitamin C, minerals, and probiotics are added to boost immune response. Pond hygiene—removing uneaten feed and bottom sludge—gets extra attention to prevent toxic gas buildup.

These are real operational costs. They do not make supply disappear, but they can slow growth cycles and modestly reduce output during peak heat months—which happen to coincide with H2 sourcing windows.

See more: Top Pangasius Importer Markets 2025 & 2026 Outlook

Rising Input Costs and Farmer Hesitancy to Restock

Pangasius production costs have risen to $1.20–$1.30 USD per kilogram, driven by feed prices, energy, and the cost of the climate-adaptation measures described above. When farmgate prices do not keep pace, some farmers hesitate to restock ponds after harvest.

This hesitancy creates a potential lag in supply. If demand surges (say, because every whitefish buyer simultaneously discovers pangasius is cheaper than cod), the farming sector needs lead time to respond. Pangasius reaches harvest size in roughly 6–8 months, so decisions farmers make today about restocking directly affect supply availability in late 2026 and early 2027.

For importers, the practical takeaway is this: lock in relationships and forward commitments early rather than trying to spot-buy into a tightening market.

Salinity Intrusion and Long-Term Adaptation Strategies

Climate change is pushing saltwater further into the Mekong Delta’s freshwater farming zones. This is not an immediate crisis for most current farming areas, but it is a structural trend that the industry is actively addressing.

Authorities in Can Tho are piloting salinity-tolerant pangasius farming programs, designating zones for brackish-water aquaculture and integrating recirculating aquaculture systems (RAS) to reduce water exchange and control waste. These initiatives are still early-stage, but they signal that Vietnam’s pangasius sector is thinking long-term about climate resilience—a factor that should give importers confidence about medium-term supply security.

What This Means for Seafood Importers Sourcing in H2 2026

Let us step back and connect the dots.

Wild whitefish supply is constrained across all major species. Cod is up 40 percent. Pollock yields are down nearly 20 percent. Haddock offers only partial relief at still-elevated prices. These are not temporary blips—they reflect quota reductions, biological cycles, and regulatory tightening that will persist through at least the remainder of 2026.

Vietnam pangasius offers a scalable, cost-competitive, and increasingly quality-differentiated alternative. It is not a perfect one-to-one substitute for premium cod applications, but for coated, prepared, institutional, and price-sensitive retail segments, it fills the gap convincingly.

The window to act is now. Waiting until Q3 or Q4 to scramble for pangasius supply means competing with every other importer who just reached the same conclusion.

Practical Sourcing Checklist for Importers

Here is a quick reference to guide your H2 2026 pangasius sourcing:

- Verify certifications early. ASC, BAP, GlobalG.A.P.—confirm what your target market and retail partners require. Our complete importer’s guide details the certification landscape.

- Assess value-added capabilities. If you are replacing cod in breaded or coated products, confirm your supplier can deliver the specific formats (portion cuts, marinated, IQF) you need.

- Discuss forward contracts. With input costs rising and farmer restocking uncertain, spot pricing may be volatile. Locking in volumes and pricing for H2 gives both parties planning certainty.

- Monitor weather and water conditions. Ask your suppliers about current pond conditions, mortality rates, and feed adjustments. Transparent suppliers will share this information readily.

- Evaluate logistics lead times. Shipping schedules from Vietnam to major consuming markets can shift. Build buffer time into your delivery windows, especially for Q3 orders.

- Diversify within the category. Consider sourcing from multiple Mekong Delta provinces and processors to reduce single-point-of-failure risk.

Conclusion – A Strategic Moment for Pangasius as Whitefish Alternative

Markets create opportunities when they break old patterns. The simultaneous tightening of cod, pollock, and haddock supply in 2025–2026 is exactly that kind of pattern break. Buyers who have historically treated pangasius as whitefish alternative only reluctantly—or only for their lowest-tier product lines—now have compelling economic reasons to reconsider.

Vietnam’s pangasius industry is better positioned than it has ever been: production is stable, export infrastructure is mature, value-added processing is expanding, and the sector is actively investing in climate resilience. None of this means the challenges are trivial. Heat stress, rising costs, and salinity intrusion are real. But they are manageable risks, not disqualifying ones.

At VNSeafoodInsider, we believe the importers who move early—building relationships, securing supply, and diversifying their whitefish portfolios now—will be the ones best insulated against whatever the wild fisheries throw at us next.

The cod market just handed pangasius its best sales pitch in years. The question is whether you are ready to listen.