Vietnam’s Pangasius Export Performance in 2025

Before we dissect individual markets, let’s establish the baseline. The Vietnamese pangasius export sector didn’t just survive 2025—it thrived in its own measured way.

The headline figure tells a success story: $2.2 billion in total export value, representing an 8% increase compared to 2024. In an industry where growth often comes in fits and starts, maintaining upward momentum despite global uncertainties is no small achievement.

December alone brought in $200 million, a solid 10% bump versus December 2024. This year-end surge wasn’t just seasonal noise—it reflected genuine demand across multiple markets as importers restocked for early 2026.

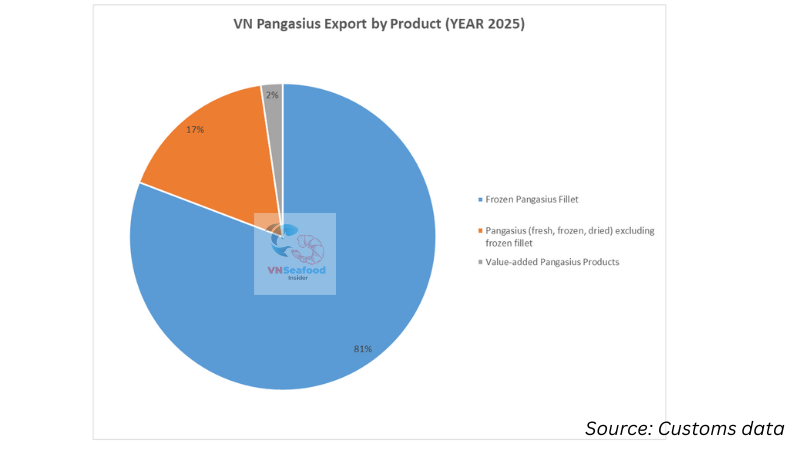

Now, not all products performed equally. The breakdown by HS codes reveals where the real action happened:

Fillet products (HS 0304) dominated the landscape with $1.8 billion in exports, growing 9% year-over-year. This category remains the workhorse of Vietnam’s pangasius industry, accounting for roughly 82% of total export value. Importers worldwide continue to prefer convenient, ready-to-cook frozen fillets that fit modern retail and foodservice needs.

Whole and steak fish (HS 03, excluding 0304) generated $377 million, essentially flat with a marginal 0.7% decline. This segment serves more traditional markets and processing facilities that prefer whole fish for further fabrication.

The most intriguing category? Value-added products (HS 1604) hit $51 million with 8% growth. While still a small slice of the pie at just over 2% of total exports, this segment represents the future. Think marinated fillets, breaded portions, and ready-to-eat products that command premium prices.

The key insight here for pangasius importer markets: Vietnam’s supply chain continues to mature, but the industry still has room to move upmarket. If you’re sourcing only commodity fillets, you’re missing opportunities in the value-added space.

See more: Pangasius Fillet Grading: What Importers Must Know

Top Pangasius Importer Markets: 2025 Winners and Losers

The global pangasius importer markets landscape shifted dramatically in 2025. Some regions doubled down on Vietnamese pangasius, while others pulled back. Understanding these dynamics isn’t just academic—it directly impacts your sourcing strategy and competitive positioning.

Let’s break down each major market and what the numbers really mean for you.

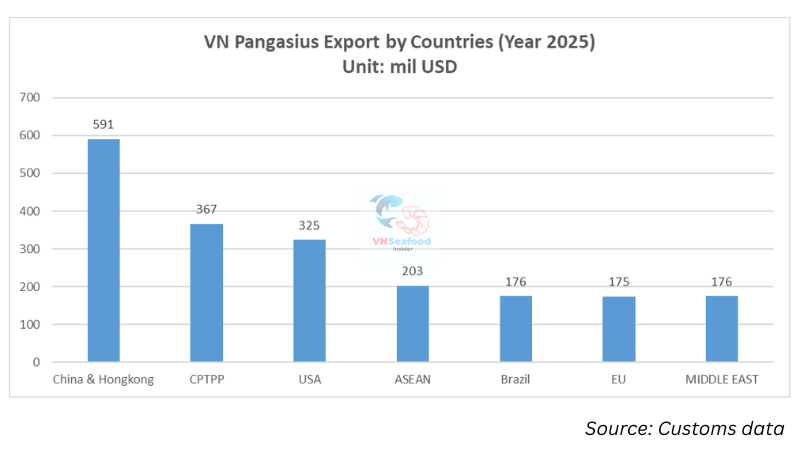

China (Including Hong Kong) – The Steady Leader

China, including Hong Kong, maintained its position as the largest single destination for Vietnamese pangasius with $591 million in 2025, up 2% from the previous year. This might look modest compared to other markets, but consistency matters.

Here’s what caught our attention at VNSeafoodInsider: December 2025 showed a remarkable surge. That month alone brought $60 million in exports, jumping 25% year-over-year and representing nearly 30% of all pangasius exported that month.

What’s driving this pattern? Year-end stockpiling behavior is deeply embedded in Chinese business culture. Importers and distributors build inventory ahead of Lunar New Year demand, creating predictable seasonal spikes.

The Chinese pangasius market appreciates product versatility. Unlike some Western markets focused exclusively on fillets, Chinese consumers and processors utilize both fillet and whole fish across diverse applications—from restaurant hotpots to retail frozen sections.

For frozen pangasius fillet suppliers, China represents stability rather than explosive growth, but in volatile times, stability has real value.

United States – Facing Headwinds

Let’s address the elephant in the room: the US market struggled in 2025, and 2026 doesn’t look much brighter.

Total imports reached $325 million, down 6% from 2024. More concerning? December’s performance showed a dramatic 37% year-over-year decline to just $17 million. That’s not a blip—it’s a trend with serious implications.

The culprit is straightforward: a 20% countervailing duty imposed on Vietnamese pangasius has fundamentally altered the competitive landscape. Add persistent high inventory levels carried by US importers from previous periods, and you’ve got a perfect storm suppressing new orders.

What does this mean for you? If you’re a pangasius importer focused primarily on the US market, diversification isn’t optional anymore—it’s survival. The math simply doesn’t work when a 20% duty eliminates your margin advantage over competing proteins like tilapia or domestic catfish.

US importers themselves are caught in a squeeze. They’re facing price pressure from retailers and foodservice operators who won’t absorb the duty increases. Meanwhile, Vietnamese suppliers can’t reduce prices indefinitely without sacrificing quality or going underwater financially.

Recovery in early 2026? We’re skeptical. Until inventory levels normalize and duty structures change, expect continued weakness.

Brazil – The Breakout Star

If the US story is cautionary, Brazil’s trajectory is downright exciting.

Brazilian imports of Vietnamese pangasius hit $176 million in 2025, exploding 36% year-over-year. December alone saw $18 million imported, representing a staggering 65% increase versus December 2024.

Why is Brazil booming? Several factors converge:

First, Brazil’s growing middle class is consuming more protein overall, and frozen pangasius fillet offers exceptional value relative to local alternatives like native catfish species or imported options from other origins.

Second, Vietnamese pangasius quality has won over Brazilian importers and consumers. The consistent sizing, clean white flesh, and mild flavor profile fit perfectly with Brazilian cooking preferences.

Third, competitive pricing matters. While raw material costs have increased globally, Vietnamese pangasius remains more affordable than many competing white fish proteins in the Brazilian market.

For pangasius exporters looking at 2026, Brazil represents the single best growth opportunity. Market penetration is still relatively early-stage, meaning substantial upside remains as distribution expands beyond major urban centers into secondary cities.

CPTPP Countries – Strategic Growth Zone

The Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) member countries collectively imported $367 million of Vietnamese pangasius in 2025, surging 34% versus 2024.

This isn’t one market—it’s a diverse collection of economies benefiting from preferential tariff treatment that makes Vietnamese pangasius significantly more competitive.

Let’s spotlight the top performers:

Mexico led CPTPP imports at $77 million, establishing itself as a major pangasius consumer. The Mexican market particularly values fillet products for retail and restaurant applications.

United Kingdom imported $60 million, with December showing 12% growth as the post-Brexit trade environment stabilizes. The UK represents a mature market with sophisticated quality and sustainability requirements.

Colombia contributed $56 million, demonstrating that Latin American markets beyond Brazil are waking up to pangasius opportunities.

Japan showed promising December momentum with $4 million, up 33% year-over-year. While still smaller in absolute terms, Japanese growth is particularly valuable given the market’s premium positioning and high standards.

December’s overall CPTPP performance jumped 30% year-over-year, suggesting accelerating rather than slowing momentum heading into 2026.

The strategic advantage? Preferential tariff rates under CPTPP mean Vietnamese pangasius suppliers enjoy better pricing versus competitors from non-member countries. If you’re sourcing for CPTPP markets, Vietnamese origin delivers tangible cost benefits.

ASEAN – Regional Integration Pays Off

Sometimes the best opportunities are closest to home. ASEAN countries imported $203 million of Vietnamese pangasius in 2025, up 20% from the prior year.

December brought $16 million in exports, an 8% year-over-year increase that reflects steady, sustainable demand.

Regional integration and reduced trade barriers make intra-ASEAN pangasius trade increasingly efficient. Lower logistics costs and cultural familiarity with the product drive consistent consumption across multiple applications—from street food to hotel restaurants to retail frozen sections.

For pangasius importers within ASEAN, proximity to Vietnamese production provides supply chain advantages that distant markets can’t match: shorter transit times, fresher products, and greater flexibility in order quantities.

Middle East – Steady Expansion

The Middle Eastern market delivered $176 million in pangasius imports during 2025, growing 19% year-over-year. December contributed $16 million, up 8% versus the prior year.

This region particularly values halal-certified products, and Vietnamese pangasius export facilities have increasingly obtained necessary certifications to serve this market effectively.

The Middle East offers demographic tailwinds: growing populations, rising incomes, and increasing protein consumption per capita. As a relatively affordable, sustainable white fish option, pangasius fits multiple consumption occasions.

European Union – Stabilizing After Decline

The EU market imported $175 million of Vietnamese pangasius in 2025, essentially flat with a marginal 0.5% decline from 2024.

However, December told a more optimistic story: $16 million in exports represented 2% year-over-year growth, the first positive monthly comparison in several quarters.

The EU remains challenging for pangasius exporters. Stringent sustainability requirements, complex regulatory frameworks, and consumer price sensitivity create barriers. Yet the year-end uptick suggests the market may be stabilizing after a period of adjustment.

For importers serving EU markets, differentiation through sustainability certifications (ASC, BAP) and value-added products becomes essential rather than optional.

See more: Top 20 biggest seafood companies in vietnam

What Pangasius Importers Need to Know About Supply Dynamics

Understanding market demand is only half the equation. Supply-side dynamics will significantly impact your 2026 strategy, especially if you’re locking in contracts now.

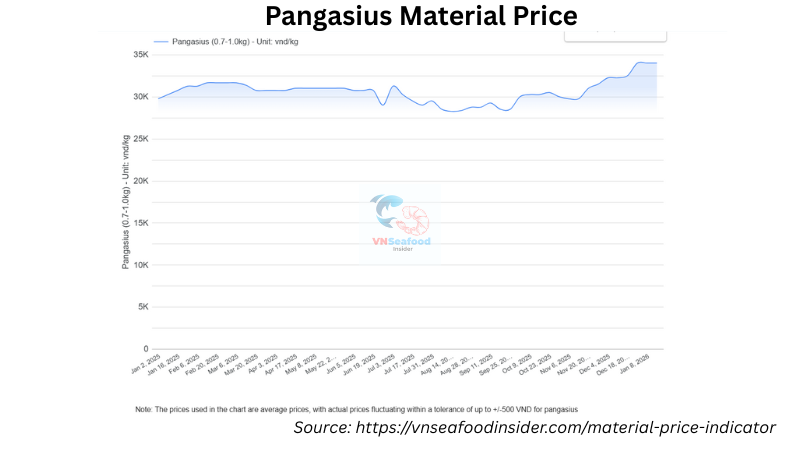

Here’s the reality Vietnamese frozen pangasius fillet suppliers are facing: raw material costs have increased substantially and supply tightness isn’t going away quickly.

Current pricing for the popular 800-1000 gram fish size sits at 33,000-35,000 VND per kilogram, representing a 15% increase compared to just 2-3 months ago. That’s not a seasonal fluctuation—it reflects genuine supply shortage pressures.

Fingerling prices tell a similar story: 80,000-85,000 VND per KG. It doubled number compared to the same period of last year.

What’s causing the squeeze? Several factors compound:

Weather patterns affecting grow-out cycles, increased disease pressure in some farming regions, and farmers’ cautious restocking behavior following earlier periods of low farm-gate prices all contribute to current supply tightness.

For pangasius importers, this creates specific implications:

Price pressure will continue through Q1 2026 at minimum. Don’t expect rapid cost relief. The biological cycle of pangasius farming means today’s fingerling shortage translates to harvest-size fish shortages 6-8 months downstream.

Securing relationships with reliable suppliers is more critical than ever. When supply tightens, suppliers prioritize long-term partners over spot buyers. If you’re sourcing on a purely transactional, lowest-price basis, you may find yourself without adequate supply when you need it most.

Early contracting may lock in relatively better rates. As more buyers recognize supply constraints, competition for available volume will intensify. Forward contracts signed now—even at elevated prices—may look smart if spot markets rise further.

The supply dynamic also affects product mix. Premium sizes and specifications may face tighter availability than standard offerings. Building flexibility into your product requirements helps ensure consistent supply access.

Pangasius Export Forecast 2026: Opportunities and Challenges

Crystal balls are notoriously unreliable, but data-driven analysis can paint a realistic picture of what’s ahead. The pangasius export forecast 2026 requires looking at both headwinds and tailwinds.

Major Challenges Ahead

Let’s start with reality: significant obstacles remain.

The US market pressure isn’t resolving quickly. That 20% countervailing duty fundamentally changed cost structures. December’s 37% decline signals this isn’t temporary weakness—it’s structural adjustment. US-focused importers and suppliers will continue struggling through at least the first half of 2026.

Alternative sourcing strategies become essential. If your business model depends heavily on US volumes, you’re playing a losing game unless you diversify geography or move upmarket into products where the duty impact is less determinative.

Supply-side constraints will limit growth capacity. Remember those elevated raw material costs (+15%)? They’re squeezing margins across the value chain. Some smaller producers may reduce operations or exit entirely, potentially tightening supply further.

Quality frozen pangasius fillet suppliers will increasingly prioritize long-term contracts with reliable buyers over spot market opportunities. This shift toward relationship-based rather than purely transactional business benefits established players but creates challenges for new entrants or opportunistic buyers.

See more: Top 5 exotic vietnam white fish that the importers should consider

Growth Opportunities for Pangasius Importers

Now the good news: substantial opportunities exist for those positioned to capitalize.

Diversification into high-growth markets represents the clearest path forward. Brazil’s 36% growth trajectory isn’t slowing—it’s accelerating. CPTPP markets’ 34% surge reflects structural advantages from preferential tariffs. ASEAN’s 20% growth and the Middle East’s 19% expansion show consistent momentum.

The strategic recommendation? Reduce US dependency and aggressively pivot toward emerging markets. For pangasius importers willing to invest in understanding new markets’ specific requirements, distribution channels, and consumer preferences, first-mover advantages remain available.

Value-added product potential remains largely untapped. HS 1604 products grew 8% to reach $51 million—but that’s only 2.3% of total exports. Compare that to other seafood categories where processed products often represent 15-25% of export value, and the opportunity becomes clear.

What types of products? Marinated fillets in various flavor profiles, breaded and battered portions ready for frying, pre-seasoned options for grilling, portion-controlled packs for foodservice, and fully cooked ready-to-eat items for retail.

Importers seeking differentiation and higher margins should work with Vietnamese pangasius export facilities capable of custom product development. The market rewards innovation, and processing capabilities in Vietnam continue improving.

Sustainability certifications transition from nice-to-have to must-have, especially in developed markets. EU buyers increasingly require ASC, BAP, or equivalent certifications. Some retailers won’t even consider non-certified products.

For importers, this means verifying your supplier credentials thoroughly. Don’t rely on promises—validate actual certificates, understand scope and expiration dates, and ensure traceability systems meet your market requirements.

2026 Outlook Summary

Putting it all together, what’s realistic for 2026?

Our conservative forecast projects $2.2-2.4 billion in total Vietnamese pangasius exports, representing 0-9% growth. This assumes continued US weakness partially offset by strong performance in Brazil, CPTPP, and other emerging markets.

An upside scenario exists if Brazil and CPTPP markets exceed expectations and EU stabilization accelerates. In this case, total exports could push toward $2.5 billion, representing 13-14% growth.

Downside risks center on further US deterioration beyond current projections, supply constraints more severe than anticipated limiting export capacity, or unexpected trade policy changes in major importing countries.

The strategic imperative for 2026 is unambiguous: market diversification is essential. Single-market dependency—regardless of which market—creates unacceptable risk in the current environment.

Is Your Country Missing Out? Strategic Recommendations

Different markets require different strategies. Here’s what VNSeafoodInsider recommends based on your position.

For importers in declining markets (US, EU): Negotiate aggressively on pricing. Suppliers facing volume declines in these markets need your business, giving you leverage. Consider bypassing intermediaries to establish direct manufacturer relationships, reducing costs and improving margins. Explore value-added products that can command premium pricing to offset duty impacts or price pressure.

For importers in growth markets (Brazil, CPTPP, ASEAN, Middle East): Lock in supply agreements early, before capacity tightens further. Build strategic partnerships with certified Vietnamese suppliers—relationships matter when supply is constrained. Capitalize on growing consumer acceptance by expanding distribution, introducing new product forms, and investing in market development.

For new market entrants: Vietnam’s $2.2 billion pangasius importer markets offer proven supply reliability—this isn’t an unproven commodity. Competitive pricing versus tilapia, cod, and other white fish creates clear value propositions for price-conscious consumers. A diversified supplier base reduces concentration risk compared to sourcing from single-country alternatives.

Specific action items regardless of your market:

Assess current supplier certifications and capabilities honestly. Are they positioned for increasingly stringent sustainability requirements? Do they have processing flexibility for value-added products?

Evaluate tariff implications for your specific market. CPTPP advantages, US duties, and various preferential trade agreements create vastly different cost structures.

Consider product mix beyond basic frozen fillets. Margins are compressing on commodity products; differentiation increasingly happens through value-added offerings.

Conclusion

Vietnam’s pangasius export industry delivered resilience in 2025 with $2.2 billion in total shipments, proving this protein’s staying power in global markets despite significant challenges.

The story of 2025—and the preview of 2026—is market divergence. Brazil and CPTPP countries surged dramatically while the US contracted. This isn’t just statistical noise; it represents fundamental shifts in global trade patterns, regulatory environments, and consumer preferences.

Looking toward 2026, we’re cautiously optimistic with significant market-specific variations. Pangasius importers who adapt strategies to these shifting dynamics—diversifying geography, moving up the value chain, and building resilient supplier relationships—will thrive. Those who remain rigid risk being left behind.

The Vietnamese pangasius export sector has proven its ability to adapt and grow over multiple decades. The fish that skeptics once dismissed as a low-value commodity now commands a multi-billion dollar global market. Suppliers continue improving quality, processing capabilities, and sustainability credentials.

Is your country missing the boom? Only you can answer that. But the data is clear: pangasius importer markets are expanding, diversifying, and creating opportunities for those positioned to capitalize. See full Vietnam pangasius guide.

At VNSeafoodInsider, we’ll continue tracking these trends, analyzing the data, and bringing you insights that matter for your business. The pangasius story is far from over—in many ways, it’s just getting interesting.