Vietnam Pangasius Supply Chain in 2026: A Strong Start With Growing Headwinds

Export Performance: $905 Million in Five Months, Up 12.6%

Vietnam’s pangasius exports reached $905 million in the first five months of 2026, marking a 12.6% increase year-over-year. That’s not a fluke. It reflects a genuine alignment between what pangasius offers — affordable, versatile whitefish — and what global consumers currently need: protein that doesn’t break the bank.

The growth wasn’t concentrated in one place, either. China continued absorbing significant volumes. ASEAN markets showed a steady appetite. The Middle East kept ordering. The EU, despite its labyrinth of compliance requirements, remained a reliable destination. And several emerging markets began placing orders that, while modest individually, added up to meaningful volume.

The full-year forecast sits around $2.3 billion, and based on H1 momentum, that target looks achievable — if the second half cooperates. That’s a big “if.”

Why the Pangasius Supply Chain Faces a Critical H2 Test

Here’s where VNSeafoodInsider needs to level with you. Three pressure points are converging as we head into the second half of 2026, and each one deserves your attention:

First, raw material prices have dropped — which sounds great until you understand why, and how long it might last.

Second, the US market is sitting on high inventory while a new federal investigation adds regulatory uncertainty.

Third, logistics costs are surging, with peak season surcharges threatening to eat into margins that were already thin.

If you’re an importer or distributor reading this, the next few sections are essentially your weather forecast for H2. Pack accordingly.

Raw Material Prices Drop — What’s Behind the Shift?

Price drops in any supply chain tend to trigger one of two reactions: celebration or suspicion. In the case of Vietnam pangasius raw material price 2026, a healthy dose of both is warranted. Prices have genuinely eased. But the reasons behind that easing reveal something important about what comes next.

Fingerling Prices Fall From Peak: From 80,000 to 48,000–52,000 VND

Remember when fingerling prices hit 70-80,000 VND per piece? That was late 2025, and it scared a lot of farmers out of expansion plans. At that price, the math simply didn’t work for smaller operations. Many chose to wait rather than stock new ponds.

Fast forward to mid-2026, and fingerlings have dropped to 48,000–52,000 VND. That’s a significant correction — roughly 37% off the peak. What does this tell us? It signals that breeding operations have caught up with demand, at least temporarily. More fingerlings available means more fish in ponds six to eight months from now, which theoretically means more raw material supply entering the processing pipeline in early 2027.

But — and this is crucial — it doesn’t mean farmers are rushing back in. Feed costs remain elevated. Transport isn’t getting cheaper. The caution that was set in during 2025 hasn’t fully been lifted. Think of it as a market that’s exhaling, not inhaling.

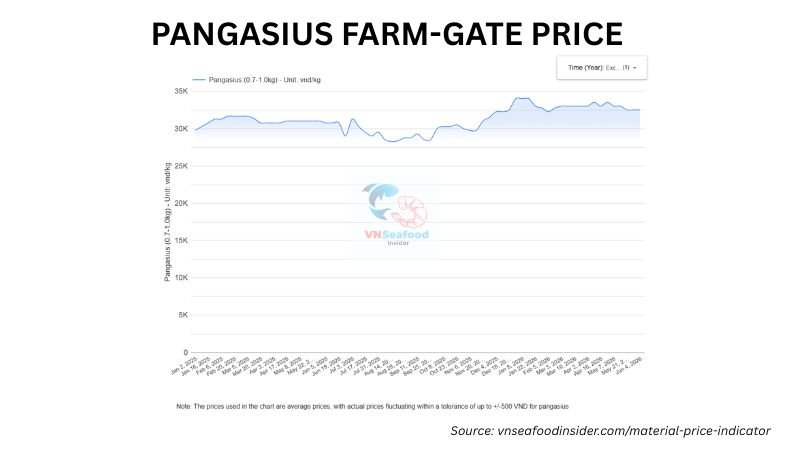

Raw Fish Price Eases to 31,500–32,000 VND/kg — The “Favorable Nursing Season” Effect

If you’ve spent time around the Mekong Delta, you’ve probably heard the phrase “mùa thuận ương.” For those who haven’t — and there’s no reason you would have unless you’ve stood next to a pond in An Giang at 5 AM — here’s what it means.

“Mùa thuận ương” translates roughly to “favorable nursing season.” It’s the window when environmental conditions align perfectly for raising fish from larvae to fingerlings. Water temperatures are mild. pH levels stay stable. Dissolved oxygen is plentiful. The result? Higher survival rates among young fish, which means more supply entering the chain, which means prices soften.

Raw fish prices have eased to 31,500–32,000 VND/kg, down from the 34,000–35,000 VND peak. That’s welcome relief for processors, and by extension, for you.

Here’s the catch, though. This season is exactly that — a season. It doesn’t last forever. As conditions shift heading into Q3 and Q4, the nursing advantage fades. Survival rates typically decline, supply tightens, and prices firm up. It’s a pattern as reliable as monsoon rains.

What Lower Input Prices Mean for Importers Right Now

So what should you actually do with this information?

In plain terms: this is a buying window. Raw material costs are at their lowest point of the year, and processors can offer more competitive pricing than they will in three months. If you’ve been waiting for the right moment to place H2 orders, this is about as close to a neon sign as the pangasius supply chain 2026 will give you.

But VNSeafoodInsider wants to be honest with you — don’t build your entire H2 strategy around the assumption that these prices will hold. Farm expansion remains cautious. Feed costs haven’t dropped. When the favorable nursing season ends, the math changes. The price today is not the price in October.

See more: Inside Vietnam Pangasius Farming — What Every Seafood Importer Must Know

The US Market: High Inventory and a New Compliance Risk

If the raw material picture is cautiously optimistic, the US market situation is… less so. Two distinct challenges are colliding, and together they create genuine uncertainty for any exporter with significant US exposure.

Overstocked US Buyers Are Slowing Orders in H1 2026

US distributors bought aggressively in late 2025 and early 2026. Perhaps too aggressively. Warehouse inventory levels for frozen pangasius fillets are running high across multiple distribution channels, and the natural consequence is playing out: buyers are slowing their purchase frequency.

For Vietnamese exporters, this creates a cash flow squeeze. Processing lines that were running at capacity in Q1 are now looking at softer order books. Production planning becomes a guessing game. And when American buyers do place orders, they’re negotiating harder because they know they have leverage.

It’s not a crisis — pangasius demand in the US hasn’t collapsed. But it is a hangover, and hangovers take time to clear.

USTR Section 301 Investigation: What It Means for Vietnam Seafood Exporters

Now for the part that’s keeping compliance officers up at night.

In early June 2026, the US Trade Representative invoked Section 301 of the Trade Act of 1974, launching an investigation into 60 economies — Vietnam included — for allegedly failing to enforce import bans on goods produced using forced labor. The formal terminology is measured and bureaucratic. The implications are not.

This Vietnam seafood forced labor investigation could result in heightened documentation requirements, additional scrutiny at customs, longer clearance times, and — in a worst-case scenario — targeted tariffs or import restrictions. The investigation is still in its early stages, so outcomes remain uncertain. But uncertainty itself is a cost in international trade.

If you’re a US-based importer sourcing pangasius from Vietnam, here’s VNSeafoodInsider’s straightforward advice: review your supplier compliance documentation now. Don’t wait for the investigation to produce findings. Ensure your Vietnamese suppliers can demonstrate clear labor practices, third-party audits, and transparent supply chain records. The companies that prepare proactively will navigate this far more smoothly than those who scramble reactively.

Logistics Costs Surge: Peak Season Surcharges Hit $600–$1,000 per Container

As if raw material volatility and regulatory risk weren’t enough, let’s talk about getting the fish from Point A to Point B. Because that’s getting more expensive too.

Which Shipping Lines Are Applying PSS Surcharges — and How Much

Several major carriers have announced Peak Season Surcharges (PSS) ranging from $600 to $1,000 per container, effective mid-2026. This isn’t unusual in principle — PSS surcharges are a regular feature of the shipping calendar. But the magnitude this year is notable, reflecting tight vessel capacity, port congestion in key markets, and carriers’ determination to protect their own margins.

The frozen fish fillet shipping cost 2026 picture, in short, is not pretty.

How Rising Freight Rates Impact Your Pangasius Landed Cost

Let’s put real numbers to this. A standard 40-foot reefer container holds approximately 22–24 metric tons of frozen pangasius fillets. An additional $800 surcharge (splitting the difference) adds roughly $0.03 per kilogram to your landed cost. That sounds small — until you multiply it across hundreds of containers and razor-thin margins.

VNSeafoodInsider’s practical suggestions: lock in freight rates early if your shipping contracts allow it. Consider consolidated shipments to maximize container utilization. And if your freight forwarder hasn’t proactively flagged these surcharges, it might be time for a conversation — or a new freight forwarder.

One important bit of perspective, though. Even with higher freight costs, pangasius remains substantially cheaper than cod (up roughly 40% in recent years) and haddock. The competitive gap has narrowed slightly, but it hasn’t closed. Pangasius is still the value play in the whitefish category, and that matters enormously in today’s market.

See more: Cod Prices Up 40%, Supply Down: The Case for Vietnam Pangasius as a Whitefish Alternative in H2 2026

Opportunities Amid the Pressure: Where the Pangasius Supply Chain Holds Strong

It would be easy to read everything above and conclude that the sky is falling. It isn’t. The pangasius supply chain 2026 faces real challenges, but it also holds genuine advantages that shouldn’t get lost in the noise.

China, ASEAN, and the Middle East: Markets With Room to Grow

Diversification isn’t just a buzzword — it’s a survival strategy. And Vietnam’s pangasius industry has been executing it effectively. China accounts for roughly 30% of export share and continues absorbing volume. ASEAN markets — particularly the Philippines, Thailand, and Malaysia — show consistent demand patterns. The Middle East, with its growing population and preference for affordable imported protein, represents durable long-term potential.

For exporters feeling the pinch in the US market, these alternatives aren’t consolation prizes. They’re genuine growth engines that reduce single-market dependency and provide more balanced revenue streams.

Value-for-Money Positioning: Why Pangasius Wins When Consumers Cut Budgets

Here’s a simple truth that tends to get overlooked during supply chain discussions: consumers are still struggling with the cost of living in most major markets. Grocery budgets are tight. Protein choices are increasingly driven by price per serving rather than preference.

Pangasius sits in an almost perfect position for this environment. It’s mild-flavored, versatile, easy to cook, and — crucially — affordable. When cod fillets cost two or three times as much, the consumer math does itself.

This is why VNSeafoodInsider believes importers should maintain or even expand their pangasius lines heading into H2. The demand fundamentals haven’t weakened. If anything, they’ve strengthened. The challenges are on the supply and logistics side, not the demand side. And supply-side challenges, as any seasoned trader knows, are manageable with the right planning.

H2 2026 Action Plan for Pangasius Importers and Distributors

5 Steps to Protect Your Pangasius Supply Chain in the Second Half of 2026

Enough analysis. Here’s what you should actually do.

- Book orders now while raw material prices are seasonally low. The favorable nursing season has created a window. Windows close. Use this one while it’s open.

- Lock in freight rates before PSS surcharges compound. Mid-2026 surcharges are already announced. If peak season tightens further, additional charges aren’t out of the question. Negotiate now.

- Audit supplier compliance documentation ahead of US Section 301 scrutiny. If your supplier can’t produce clear, auditable labor practice records, that’s a risk you need to address before regulators do it for you. You can check full Vietnam pangasius guide.

- Diversify destination markets beyond the US if you’re heavily concentrated there. The US inventory overhang will clear eventually, but regulatory uncertainty may linger. Don’t put all your pangasius in one basket.

- Monitor fingerling price recovery as a leading indicator of H2 supply tightness. When fingerling prices start climbing again — and they will — it’s an early signal that raw material prices will follow six to eight months later. Watch the data, not just the headlines.

The pangasius supply chain 2026 is navigating a genuinely complex moment. Prices are favorable today but unlikely to stay that way. The US market is cautious and increasingly complicated. Logistics costs are climbing. And yet, global demand for affordable whitefish has never been stronger.

The importers who thrive in H2 won’t be the ones who got lucky. They’ll be the ones who planned in advance. Contact VNSeafoodInsider— we’ll help you navigate what’s coming.