Why Vietnam Pangasius Dominates the Global White Fish Market

Before you compare suppliers or request quotes, you need to understand why Vietnam holds the position it does. This isn’t just about cheap fish. It’s about structural advantages that no competing origin has been able to replicate.

Vietnam’s Monopoly Position in Global Pangasius Supply

Here’s the number that frames everything: Vietnam controls approximately 90% of the world’s frozen pangasius fillet supply. That’s not market leadership. That’s a near-monopoly.

Annual commercial production sits between 1.5 and 1.7 million tonnes. Export revenue reached roughly $2.0 billion in 2024 and is projected to approach $2.2 billion in 2025 — an 8–10% year-on-year increase. When you buy pangasius fish on the international market, you’re almost certainly buying Vietnamese.

You may see that other countries like Bangladesh, Indonesia, India or China, also farm pangasius fish, but only for local consumption because the meat quality is not able to compete with Vietnamese pangasius.

Why the Mekong Delta Makes Vietnam Pangasius Irreplaceable

About 99% of Vietnam’s commercial pangasius farming is concentrated in the Mekong Delta provinces: Dong Thap, An Giang, Can Tho, and a handful of surrounding areas. The Mekong River system provides something money can’t easily buy — year-round warm freshwater flow, flat terrain ideal for large pond systems, and a labor force with decades of aquaculture experience.

This geographic concentration is both a strength and a vulnerability. It creates extraordinary production density, but it also means that regional disruptions — flooding, disease outbreaks, fingerling shortages — ripple through global supply fast. Importers who understand this geography make better purchasing decisions.

Vietnam Pangasius vs. Other White Fish Alternatives — A Cost-Value Comparison

Compared to cod, haddock, hake, or even tilapia, Vietnamese pangasius as whitefish alternative wins on cost almost every time. The fish reaches a market weight of 1–1.2 kg in just 7–8 months. Feed costs are lower. Domestic logistics from farm to factory are short and well-established.

The result? FOB prices that consistently undercut other white fish options, which is exactly why supermarket chains and foodservice operators across dozens of countries have adopted pangasius as their go-to affordable white fish protein. It’s not replacing premium species — it’s filling the gap where price sensitivity drives purchasing decisions.

Inside Vietnam Pangasius Farming — What Buyers Need to Understand

Knowing how the fish is produced isn’t optional knowledge for serious importers. It directly affects your supply security, pricing forecasts, and quality expectations.

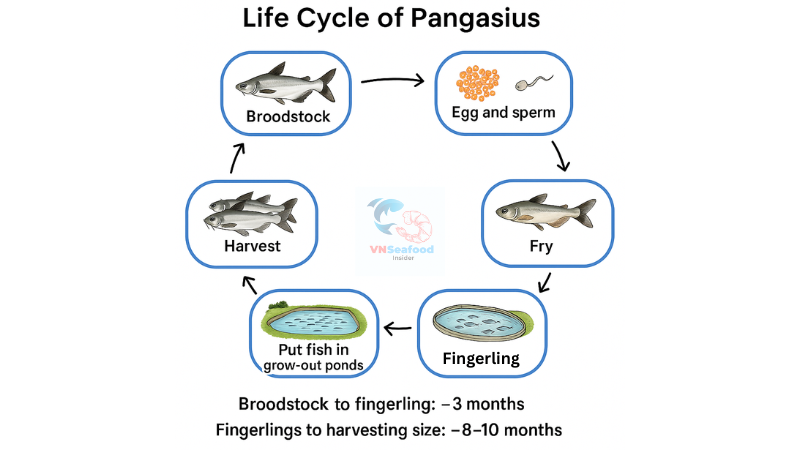

How Vietnam Pangasius Farming Works: From Fingerling to Export

The pangasius production chain has three stages. First, hatcheries produce fingerlings. Second, grow-out farms raise fish in earthen ponds over 6–8 months until they reach harvest size. Third, processing factories fillet, freeze (typically IQF or block), and pack for export.

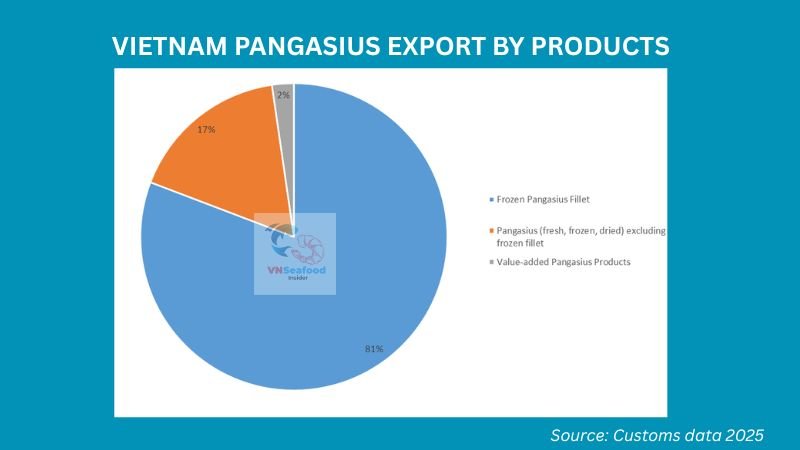

The most popular exported product is frozen pangasius fillet — skinless, in various trim levels and size ranges. The processing sector is heavily industrialized, with major factories running HACCP systems and holding multiple international certifications.

The Fingerling Shortage Problem and Its Direct Impact on Supply

This is the issue that caught many buyers off guard in 2024–2025. A severe fingerling shortage pushed seed prices to record highs, reduced stocking volumes, and tightened raw material availability heading into 2025 and early 2026.

Farm-gate prices for commercial-size pangasius (0.8–1.2 kg) reached approximately 30,000–35,000 VND/kg — around $1.2–1.4 USD/kg — levels not seen in years.

Sustainable and Certified Farming Practices — What Importers Should Look For

The certification landscape for Vietnam pangasius has matured significantly. Leading producers now hold ASC, BAP , BRC, IFS, and HACCP certifications — not as marketing badges, but as market access requirements.

EU buyers, in particular, increasingly mandate ASC or equivalent sustainability certification. Japanese and UK retailers follow similar patterns. If your target market requires a certified product, confirm this before you engage a supplier — not after the container ships.

Vietnam Pangasius Export Performance and Market Trends

Numbers tell the story better than speculation. Here’s what the data shows.

Vietnam Pangasius Export Revenue Growth: 2024–2025 in Numbers

Vietnam pangasius exports have been on a clear upward trajectory. Revenue hit approximately $2.0 billion in 2024, and the first half of 2025 showed an 11% surge compared to the same period the previous year. The full-year 2025 projection of $2.2 billion looks increasingly achievable.

This growth isn’t coming from a single market. It’s broad-based — driven by diversification across regions and product types.

Vietnam Pangasius Market Trends and Forecast for 2025–2026

Several market trends are shaping the near-term outlook. Raw material scarcity is pushing processors toward higher-value products to protect margins. Trade policy shifts — especially US tariffs — are redirecting export flows toward Latin America, the Middle East, and CPTPP markets. And rising production costs are making the old “race to the bottom” pricing model unsustainable.

For importers, the practical takeaway is this: the era of ultra-cheap pangasius is fading. Competitive pricing remains, but you’ll need to plan further ahead and commit earlier to secure supply.

Vietnam Pangasius Export Surge: Key Drivers Behind the Growth

The export surge reflects multiple converging factors. Free trade agreements — EVFTA, CPTPP, RCEP — have reduced tariff barriers in key markets. Global demand for affordable white fish protein continues to grow, particularly in emerging economies. And Vietnam’s processing sector has invested heavily in capacity, quality systems, and product diversification.

It’s a virtuous cycle, at least for now. More market access leads to more investment, which leads to better products, which opens more doors.

Top Vietnam Pangasius Import Markets — Where the Demand Is

Understanding where pangasius exports are flowing helps you benchmark your own market and spot competitive dynamics.

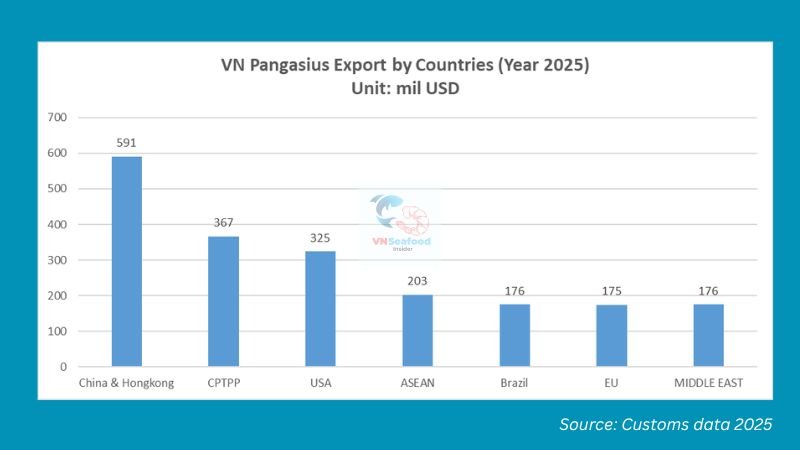

United States — Pressure From Tariffs but Still a Critical Market

The US remains a strategically important market despite ongoing headwinds. Vietnam pangasius once held over 90% of pangasius retail shelf space in America. Today, anti-dumping duties and the more recent 10% reciprocal tariff are squeezing margins and forcing importers to recalculate.

Still, the sheer size of US white fish consumption — across retail, foodservice, and QSR channels — keeps it relevant. Smart importers are adjusting product specs and pricing structures rather than abandoning the market entirely.

Brazil — The Fastest-Growing Vietnam Pangasius Importer in 2025

If there’s a breakout story in 2025, it’s Brazil. Vietnamese pangasius exports to Brazil surged approximately 73% in the first five months of 2025 compared to the same period last year. Brazilian retail and foodservice buyers are embracing frozen pangasius fillet as an affordable protein option, and the growth trajectory shows no sign of slowing.

For exporters looking to diversify away from US tariff risk, Brazil is the most compelling alternative right now.

EU, CPTPP Countries, and Emerging Markets — The New Growth Frontier

The EU continues importing tens of thousands of tonnes annually, with pangasius import values around $170–180 million. CPTPP member states — Japan, Canada, Australia, Mexico — benefit from preferential tariff rates that make Vietnamese pangasius increasingly price-competitive against locally sourced alternatives.

These markets tend to demand higher specifications and stricter certification, but they also offer more stable pricing and longer-term contracts. Worth the extra compliance effort, frankly.

China and the Middle East — Steady Volume with Long-Term Potential

China and Hong Kong represent the largest pangasius market by volume, accounting for roughly 29–32% of Vietnam’s total pangasius export value. The Middle East — particularly the UAE — offers consistent demand driven by population growth, tourism-linked foodservice, and relatively straightforward import procedures.

Neither market is flashy. Both are reliable. And in a volatile trade environment, reliability has real value.

Vietnam Pangasius Prices — How to Read the Market Before You Buy

Price is where most buying decisions start — and where most mistakes happen. Here’s how to read the pangasius price landscape intelligently.

What Drives Vietnam Pangasius Fish Price Fluctuations

Three factors dominate: fingerling availability (which determines future raw material supply), feed costs (the single largest input cost for farmers), and trade policy changes (tariffs, duties, and FTA benefits). When fingerling prices spike — as they did through 2024–2025 — everything downstream gets more expensive, with a lag of roughly 6–8 months.

Vietnam Pangasius Price Trends: From Farm-Gate to FOB

Farm-gate prices for commercial pangasius reached approximately 35,000 VND/kg ($1.4/kg) in early-to-mid 2025 — up 5,000–7,000 VND/kg from prior periods. FOB export prices depend on fillet size (130–170g, 170–220g, 220g+), trim grade (A, B, or C), treatment (phosphate-treated vs. untreated), and certification requirements.

As raw material costs have risen, many processors are shifting production toward value-added products and premium grades to protect margins. Buyers seeking the cheapest possible product may find availability tighter than expected.

How US Tariffs Are Reshaping Vietnam Pangasius Export Pricing

The combination of anti-dumping duties and the new reciprocal tariff has increased the landed cost of Vietnamese pangasius in the US significantly. This is actively redirecting trade flows — some volume that would have gone to the US is now heading to Brazil, China, the Middle East, and CPTPP markets where tariff advantages exist.

If you’re a US-based buyer, your competitive landscape just changed. If you’re buying for other markets, you may face more competition from redirected supply.

Vietnam Pangasius Quality — The Importer’s Non-Negotiable Checklist

Quality problems don’t announce themselves. They show up in your warehouse, your customer complaints, or your regulatory inspections. Prevention starts with specification.

Pangasius Fillet Grading: Color, Trim, and Size Classifications Explained

Pangasius fillet grading follows several parameters. Color should be white to light pink — yellowing or dark spots indicate quality issues. Trim levels range from un-trim (minimal cutting, fat on, red meat on, higher yield weight) through semi-trim (moderate) to well-trim (deep trim, fat off, red meat off). Size ranges typically span 120–170g, 170–220g, 220–up per piece.

Every one of these parameters affects price. Specify exactly what you need — and confirm that your supplier’s grading definitions match yours. The term “well-trimmed” means different things in different factories.

Pangasius Quality Control — The Most Common Problems and How to Avoid Them

The recurring issues VNSeafoodInsider sees importers face include: residual blood and skin on fillets, small bone fragments, inconsistent fillet thickness, and excessive drip loss after thawing. Effective quality control at the factory level requires standardized cutting procedures, optimized soaking protocols, bone-detection, and continuous microbiological monitoring.

Request third-party inspection before shipment. It costs a fraction of a rejected container.

Phosphate Treatment in Pangasius Fillets — EU Standards Every Buyer Must Know

Phosphate treatment — typically using STPP (sodium tripolyphosphate) — improves water retention and fillet appearance. However, EU regulation EC 1333/2008 requires clear labeling when phosphates are used and sets maximum permitted levels. Many European retailers now demand phosphate-free or low-phosphate products.

Specify your phosphate requirements explicitly in purchase contracts. “Standard processing” may include phosphate treatment by default unless you state otherwise.

How to Import Vietnam Pangasius — Practical Steps for Buyers

Theory is useful. Execution is what fills containers. Here’s the practical workflow.

Defining Your Vietnam Pangasius Product Specification Before Sourcing

Before contacting any supplier, document your requirements: fillet size range, trim grade, glazing percentage, treatment preferences (phosphate-free or not), packaging format (IQF, block/interleaved), certifications needed, and labeling requirements. A clear spec sheet eliminates 80% of sourcing friction.

How to Identify and Verify a Reliable Vietnam Pangasius Exporter

Start with exporters who hold relevant certifications for your target market. Verify factory audit reports (BRC, IFS, or ISO 22000). Request references from existing customers in your region. And — this matters more than most buyers realize — visit the factory if your order volume justifies it.

Certifications, Documentation, and Compliance Requirements by Market

Each destination has its own requirements. The US requires FSIS equivalence and compliance with anti-dumping procedures. The EU demands health certificates on TRACEs system, traceability documentation, and adherence to food additive regulations. CPTPP markets require certificates of origin for preferential tariff treatment.

Get the documentation right the first time. Customs delays are expensive, and rejected shipments are worse.

Frequently Asked Questions About Vietnam Pangasius

What is the difference between pangasius and basa?

Basa (Pangasius bocourti) and tra (Pangasius hypophthalmus) are both pangasius species. Virtually all commercial Vietnam pangasius production is tra. The name “basa” is sometimes used commercially in certain markets, but the product you’re buying is almost always tra.

Is Vietnam pangasius safe to eat and import?

Yes. Vietnamese pangasius exported to regulated markets like the EU, US, and Japan must pass rigorous food safety inspections, including checks for antibiotics, heavy metals, and microbiological contamination. Factories exporting to these markets operate under HACCP and hold international food safety certifications.

What fillet grades are available from Vietnamese pangasius exporters?

Standard offerings include well-trimmed, semi-trimmed, and un-trimmed fillets in sizes from 120g up to 500g+, available in IQF or block frozen formats. Value-added products like breaded fillets, marinated portions, and portion-cut pieces are increasingly available.

How does the US tariff situation affect Vietnam pangasius import costs?

Anti-dumping duties combined with the 10% reciprocal tariff significantly increase landed costs for US importers. Exact impact depends on your supplier’s specific duty rate. Factor these costs into your landed price calculations before committing to orders.

What is the minimum order quantity for importing Vietnam pangasius?

Most Vietnamese exporters work with full container loads (FCL) — typically 20–24 tons per 40-foot refrigerated container. Some trading companies offer smaller quantities, but pricing will be less competitive. For first-time buyers, starting with one container and establishing a quality baseline is standard practice.

VNSeafoodInsider publishes market intelligence, pricing analysis, and sourcing guidance for the global pangasius trade. For the latest updates on Vietnam pangasius prices, export trends, and supply conditions, explore our full coverage across the topics linked throughout this guide.